Islamabad April 9 2022: Reduced Russian diesel and gasoil exports have had a domino effect on global diesel supply chains, as European refiners scramble to replace barrels in response to Russia's military invasion of Ukraine while also looking to capture the resulting high diesel crack spreads.

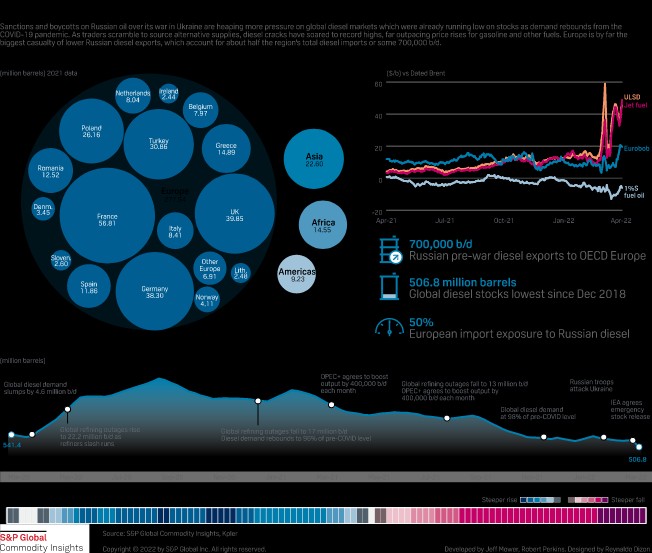

Europe has been most directly impacted by the loss of Russian diesel, having historically imported roughly 700,000 b/d of diesel from the country, amounting to 50% of Europe's total diesel imports.

After hitting an all-time high of $58.94/b March 8, the Northwest European ULSD crack spread against Dated Brent slipped to $35.21/b April 7, according to S&P Global Commodities Insights assessments.

However, that figure was up from just $5.03/b April 7, 2021, signaling a market disruption and volatility as European refiners were struggling to run at maximum capacity, which was more costly because of high natural gas and hydrogen prices.

"All refineries only produce the volume they have to for term contracts," one European trader said, thus making it difficult to find barrels on the spot market.

It has also now become more difficult to obtain feedstocks for secondary units, the majority of which are imported from Russia.

"Even on terms deal, we are told to buy only 90%," another diesel trader active in Northwest and Central Europe said.

While some Mediterranean refiners have expressed their plans to continue normal runs with the capability of readily replacing Russian crude grades, product supply has suffered as refiners shift slates and lock in crude supply.

"The [Med] market is so tight, there are no offers being shown," a third trader said.

Any additional supply was coming from other regions, including the US and Asia, traders said.

"The market has to find some way to find non-Russian origin," a second European trader said.

Global inventories low

Tight inventories for diesel across the globe have been supporting high margins, but have made it difficult to replace Russian diesel in Europe by diversifying supply sources.

Global diesel stocks were at 506.8 million barrels the week ended March 18, down from 675.5 million barrels in August 2020, when inventories surged due to low demand stemming from the coronavirus pandemic.

Global diesel demand has returned to pre-pandemic levels, but refiners have had a hard time keeping up, with the lack of Russian barrels adding to the bullish scenario.

S&P Global expected global crude distillation unit outages to average 12.13 million b/d in April before falling to 7.89 million b/d in July, which should help bring more supply to the market. In the meantime, S&P Global analysts estimated that it would take a 1% shift in global refinery yields to favor diesel to fill in the gaps.

US refiners are able to shift yields by around 2% to increase ULSD output, but that will compete with gasoline economics as the summer driving season begins.

Most recent US Energy Information Administration data showed US Gulf Coast refiners ran at 95.2% of capacity for the week ended April 1, increasing ULSD output to 2.8 million b/d, up from 2.69 million b/d the week earlier.

Flows shift

USGC refiners depend heavily on export demand and could help fill the Russian supply gap in Europe.

The US exported 1.47 million barrels of diesel and gasoil to Northern Europe in March, up from 300,000 barrels in February, Kpler data showed.

A shift in export flows from the US and Europe have raised red flags in countries that depend on imports from those regions to meet demand. Latin America, for instance, depends heavily on diesel from the US.

On March 29, a trade group for retail fuel outlets in Argentina said some stations have started rationing diesel sales because government price controls and import restrictions were discouraging refiners from bringing in enough supplies. One cause of the shortages was that government controls were keeping diesel prices 30% below import prices, a discouragement for refiners to import supplies to meet the rise in demand.

Some parts of West Africa have also been facing diesel shortfalls. The region imported 215,000 b/d of diesel in March, Kpler data showed, with Russia supplying 23,000 b/d of the total. However, so far in April, no Russian barrels have been fixed, leaving buy tenders for gasoil in West Africa without offers.

"In Africa people cannot open letters of credit if the product comes from Russia," a trader familiar with the situation said.

{kind=link}