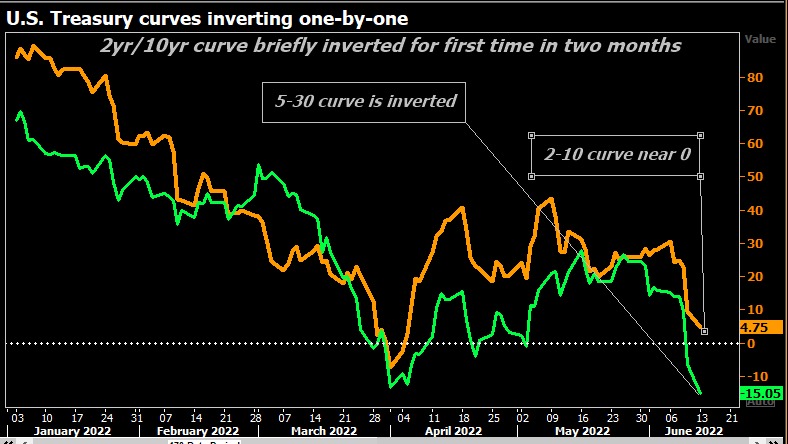

New York June 13 2022: U.S. two-year Treasury yields rose above 10-year borrowing costs on Monday – the so-called curve inversion that often heralds economic recession – on expectations interest rates may rise faster and further than anticipated.

Fears the U.S. Federal Reserve could opt for an even larger rate hike than anticipated this week to contain inflation sent two-year yields to their highest levels since 2007.

But a view is also playing out that aggressive rate hikes may tip the economy into recession.

Two-year Treasury yields rose to a 15-year high around 3.25% before easing to 3.19%, while 10-year yields touched the same level, the highest since 2018 .

Friday’s data showed the largest annual U.S. inflation increase in nearly 40-1/2 years, dashing hopes the Federal Reserve might pause its interest rate hike campaign in September. Many reckon the central bank may actually need to up the pace of tightening.

Barclays analysts said they now expected a 75 bps move from the Fed on Wednesday rather than the 50 bps which has been baked in.

Money markets are now pricing a cumulative 175 bps in hikes by September and also see a 20% chance of a 75 bps move this week, which if implemented would be the biggest single-meeting hike since 1994 .

UBS strategist Rohan Khanna said hawkish European Central Bank communication alongside the inflation print “have completely shattered this idea that the Fed may not deliver 75 bps or that other central banks will move in a gradual pace”.

“The whole idea went out the drain … that’s when you get turbo-charged flattening of yield curves. It is just a realisation that peak inflation in the U.S. is not behind us, and unless we are told so, maybe peak hawkishness from the Fed is also not behind us,” Khanna added.

Meanwhile bets on the U.S. terminal rate – where the Fed funds rate may peak this cycle – are shifting. On Monday, they priced rates to approach 4% in mid-2023, up almost one percentage point since end-May .

Deutsche Bank said it now saw rates peaking at 4.125% in mid-2023.

Some Fedwatchers are sceptical the Fed will move faster with rate hikes. Pictet Wealth Management’s senior economist Thomas Costerg noted, for instance, that most inflation drivers such as food and fuel remain outside central bankers’ control.

“Over the summer, they will be aware of growth data and housing which is starting to look more wobbly,” Costerg said. “I doubt they will do 75 bps … 50 bps is already a big step for them.”

The sell-off in Treasuries has set other markets on edge, sending German 10-year yields to the highest since 2014 and knocking S&P 500 futures 2.5% lower.

{kind=link}