London November 29 2024: An ever increasing number of UK homes are set to be passed on for free this year as homeowners seek to escape rising taxes by passing on assets to family members.

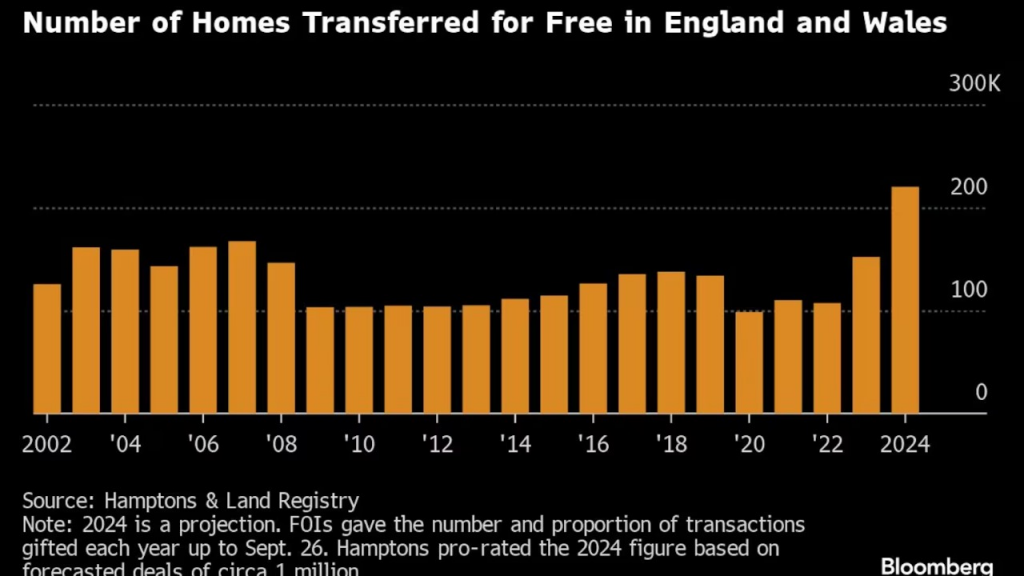

Over 220,000 homes are on course to change hands – either fully or in part – for no cash in 2024, up about 45% from last year, according to freedom of information requests by broker Hamptons submitted to the Land Registry and seen by Bloomberg. In London, more than a quarter of homes will go for nothing.

About 4 out of 10 gifted transactions in 2024 are set to involve entire properties, typically involving a parent and child. The remainder involve a share of the property in a deal often completed within generations, such as a homeowner gifting a share of their property to a non-homeowning partner.

“Rising transaction costs, particularly the higher rate of stamp duty for those who own more than one property, mean ownership is increasingly being spread across the wider family,” said David Fell, an analyst at Hamptons. He also pointed to rising council taxes for those owning more than one property, as well as higher rates of stamp duty on purchases.

In the UK, gifts can be made tax-free as long as the person passing on the assets lives for at least another seven years, making it a popular hedge against inheritance tax. However, if the person dies within that period, the recipient will have to pay tax of up to 40%. Shifting residences to close family is also a strategy to avoid paying tax on their next investment.

The so-called Bank of Mom and Dad is a growing source of finance for UK adults seeking to get on the UK’s expensive housing ladder, according to a Resolution Foundation report last week. The total value of financial gifts reached £29 billion in 2018-2020, more than double the level a decade earlier, due to a rise in both the size and numbers of gifts.

Labour’s Oct. 30 budget included a surprise two percentage point hike to stamp duty for landlords and second-home owners. The measure is the latest in a series of increases designed to deter investors and favor first-time buyers.

The data also underscores the scale of the housing crisis confronting the new Labour government after years of rampant home price inflation and a cost-of-living crisis stretched affordability. That’s likely to remain the case, with the Bank of England signaling it is in no rush to cut the cost of borrowing and an increase in employer payroll taxes threatening to translate into lower pay rises for workers.

Rampant rent inflation is also making it harder for young people to gather enough funds for a deposit without parental help. A separate Resolution Foundation report estimated it would take a typical young family over 14 years to save for a deposit, almost twice as long as in the mid-1990s.

Hamptons says rising homeowner rates after the Second World War have also left older generations holding record amounts of real estate, which are now increasingly being passed on.

“Property tax rates have steadily crept up, making the sale or purchase of a second property more expensive,” Hamptons’ Fell said. Gifting has also been “accelerated by higher capital gains tax rates and lower tax-free allowances for anyone selling a second home, making gifting it to a family member an increasingly attractive proposition,” he added.

{kind=link}